Navigating the Medicare maze can feel like hacking into a mainframe. You’re faced with a dizzying array of options, each promising comprehensive coverage. One particular program, AARP Medicare Supplement Plan G, often emerges as a top contender. But what exactly is it, and how does it work? This deep dive explores the core components of the AARP-endorsed Medigap Plan G, providing you with the information necessary to make informed decisions about your healthcare future.

AARP Medicare Supplement Plan G, offered through UnitedHealthcare (AARP plans are insured by UnitedHealthcare Insurance Company), is designed to fill the gaps in Original Medicare (Parts A and B) coverage. Imagine it as a safety net, catching the out-of-pocket expenses that Medicare doesn't cover, like copayments, coinsurance, and deductibles. This supplementary coverage provides a predictable, manageable healthcare budget, shielding you from potentially significant medical bills.

The history of Medigap plans, including Plan G, is rooted in the desire to make healthcare more affordable and accessible for seniors. As healthcare costs rose, the gaps in Original Medicare became more apparent. Medigap plans evolved to address these gaps, offering varying levels of coverage. Plan G, known for its comprehensive protection, emerged as a popular choice for those seeking peace of mind regarding their medical expenses.

Understanding AARP's role is crucial. AARP doesn't directly provide insurance; they endorse plans offered by UnitedHealthcare. This endorsement leverages AARP's reputation for advocating for seniors, giving beneficiaries a sense of trust and reliability. The importance of Plan G lies in its broad coverage. It offers protection against high out-of-pocket costs, providing financial stability and access to necessary medical care without worrying about unexpected bills.

A common issue with Plan G, and Medigap plans in general, is understanding the various options available and selecting the best fit for individual needs. The sheer volume of information can be overwhelming. This is where careful research and consultation with knowledgeable resources become essential. Navigating this landscape requires a clear understanding of your healthcare priorities and budget.

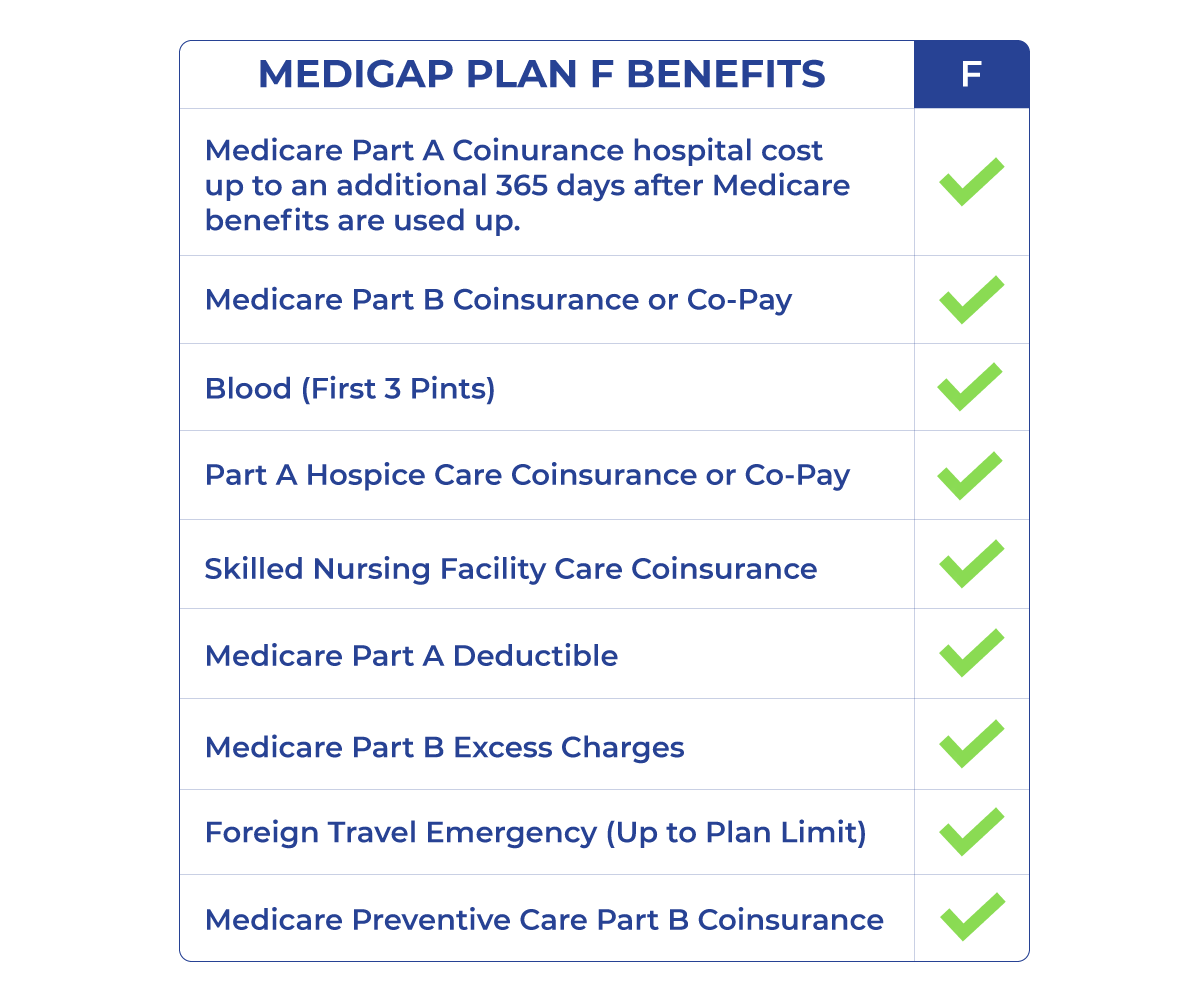

AARP Plan G covers the Medicare Part A deductible, Part B coinsurance or copayment, Part A hospice care coinsurance or copayment, skilled nursing facility care coinsurance, the first three pints of blood used in a medical procedure, Part B excess charges, and foreign travel emergency (up to plan limits). It does not cover the Part B deductible. For example, if you have a hospital stay, Plan G would cover the Part A deductible, leaving you responsible only for any costs exceeding Medicare’s approved amount.

Three key benefits of AARP Plan G are predictable costs, access to any Medicare-approved doctor or hospital, and peace of mind knowing you're protected from high out-of-pocket expenses. For instance, if you need specialized care, you can choose any doctor who accepts Medicare without worrying about network restrictions. This flexibility and financial protection offer a significant advantage.

Advantages and Disadvantages of AARP Plan G

| Advantages | Disadvantages |

|---|---|

| Comprehensive coverage | Higher premium than some other Medigap plans |

| Predictable out-of-pocket costs | Doesn't cover the Part B deductible |

| Freedom to choose any Medicare-approved doctor or hospital |

Five best practices for implementing an AARP Plan G include comparing plans, understanding your healthcare needs, checking your eligibility, enrolling during the Medigap Open Enrollment Period, and reviewing your coverage annually.

Frequently Asked Questions about AARP Plan G:

1. What is the difference between Medicare Advantage and a Medigap plan? Medicare Advantage plans are an alternative to Original Medicare, while Medigap supplements Original Medicare.

2. How do I enroll in AARP Plan G? You can enroll through a licensed insurance agent or directly through UnitedHealthcare.

3. When can I enroll in a Medigap plan? The best time is during your Medigap Open Enrollment Period.

4. Does Plan G cover prescription drugs? No, you’ll need a separate Part D prescription drug plan.

5. Can I switch Medigap plans? Yes, but you may undergo medical underwriting.

6. What is the cost of AARP Plan G? Premiums vary based on location and other factors.

7. Does AARP Plan G cover vision or dental? No, it primarily covers expenses related to hospital and medical services.

8. Where can I find more information about AARP Plan G? Contact UnitedHealthcare or visit their website.

Tips for navigating the complexities of AARP Plan G include consulting with a licensed insurance agent, comparing plans from different insurers, and reviewing your healthcare needs annually. These steps will help ensure your coverage aligns with your changing circumstances.

In conclusion, AARP Medicare Supplement Plan G offers significant benefits for those seeking comprehensive coverage and predictable healthcare costs. It provides a strong safety net against the financial burdens of unexpected medical expenses, allowing you to focus on your health and well-being. While the plan comes with a higher premium than some other Medigap options, the extensive coverage and freedom to choose any Medicare-approved doctor often outweigh the cost for many beneficiaries. Understanding the nuances of Plan G is crucial for making an informed decision. Researching, comparing plans, and seeking professional advice will empower you to choose the best coverage for your individual needs and ensure a secure healthcare future. Take control of your healthcare journey – explore the possibilities and secure the coverage you deserve. Don’t hesitate to reach out to resources like UnitedHealthcare and Medicare.gov for more information.

Jefferson county jail inmate search guide

Unleash the bass connecting 4 subwoofers for maximum impact

Transform your home with sherwin williams exterior house stains