Choosing the right Medicare coverage can feel like navigating a maze. One option many seniors consider is a Medicare Supplement plan, also known as Medigap. Among these plans, Plan F, often offered through organizations like AARP, has historically been a popular choice. But what exactly is AARP's Plan F, and is it the right fit for you?

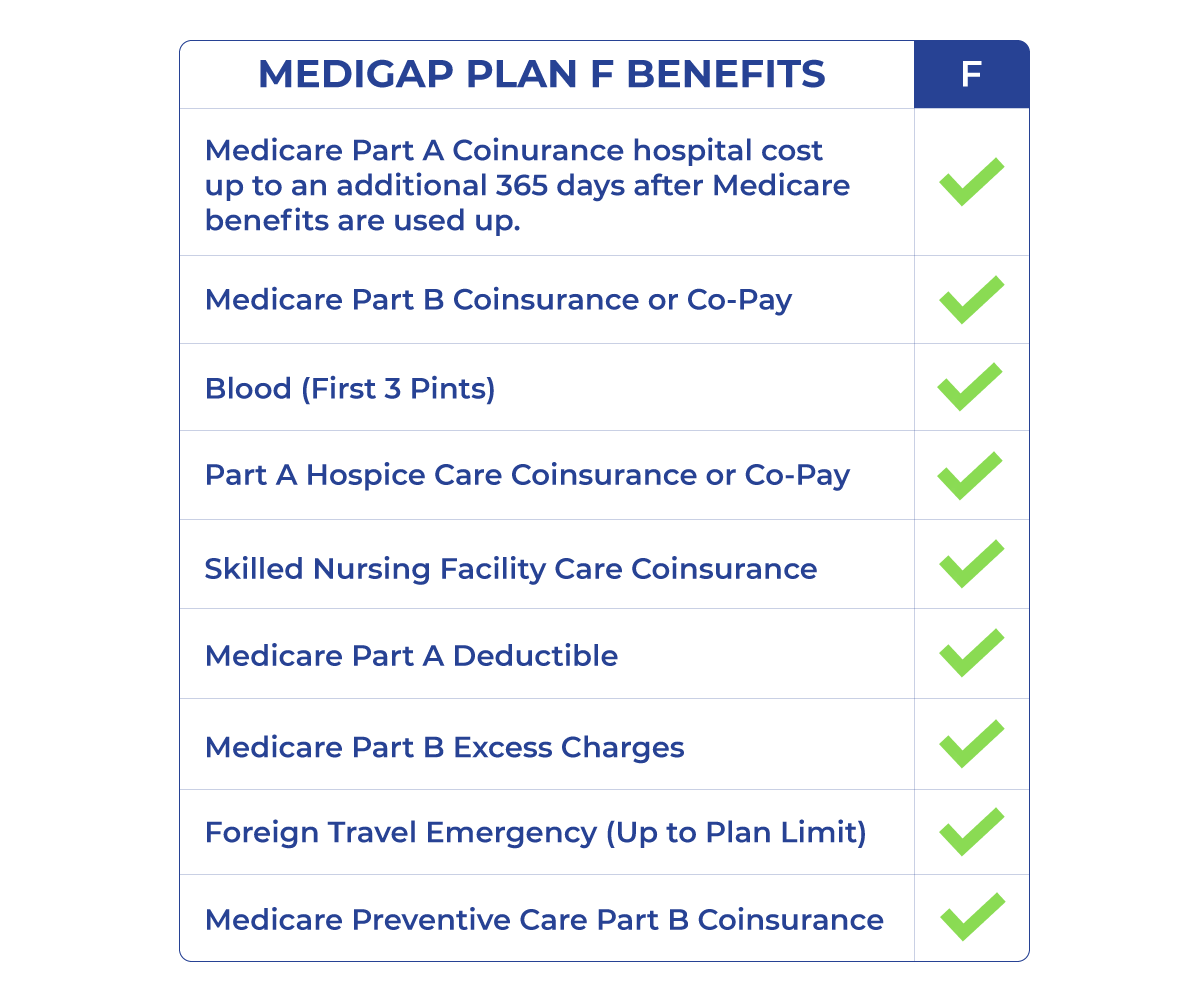

Medicare Supplement Plan F, offered by AARP and other insurance providers, is designed to help fill the “gaps” in Original Medicare (Parts A and B) coverage. These gaps include things like copayments, coinsurance, and deductibles. Before 2020, Plan F was known for its comprehensive coverage, picking up virtually all out-of-pocket costs associated with Original Medicare. This made it a very attractive option for those seeking predictable healthcare expenses.

The history of Medigap plans like Plan F is intertwined with the evolution of Medicare itself. As Medicare evolved, so did the need for supplemental coverage to address its cost-sharing structure. Plan F emerged as a key player, offering significant financial protection for beneficiaries. However, changes to Medicare law in 2019 impacted the availability of Plan F for newly eligible beneficiaries starting in 2020. Individuals who were already enrolled in Plan F before this date could maintain their coverage.

The significance of Plan F lies in its comprehensive coverage. It provided a sense of security, knowing that most, if not all, out-of-pocket expenses would be covered. This is particularly important for individuals with chronic health conditions or those who anticipate high healthcare utilization. The main issue surrounding Plan F now is its limited availability to new Medicare beneficiaries. This has led to discussions about alternative Medigap options, like Plan G, which offers similar coverage with the exception of the Part B deductible.

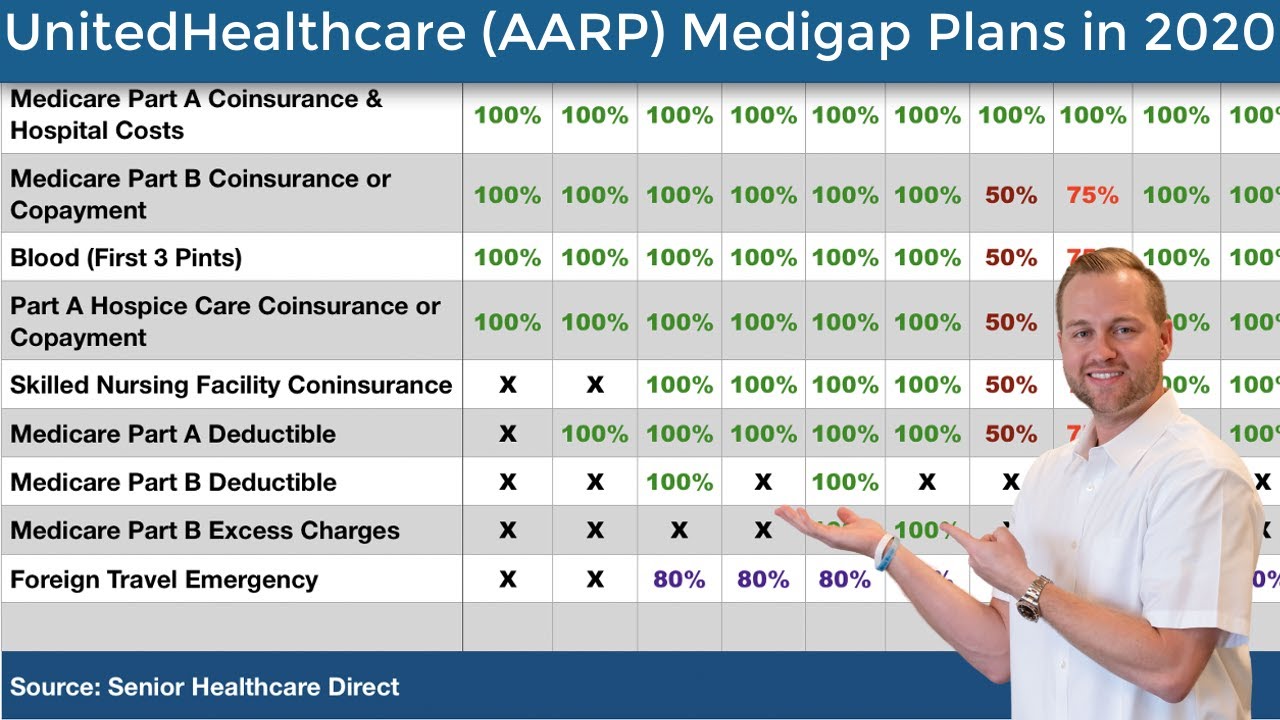

Understanding AARP's role is also crucial. While AARP doesn't directly underwrite insurance, it endorses plans from UnitedHealthcare, a leading insurance provider. When you see "AARP Medicare Supplement Plan F," it refers to a Plan F policy offered by UnitedHealthcare under the AARP brand. This association often provides a sense of trust and reliability for many seniors.

While Plan F is no longer available to newly eligible Medicare beneficiaries, those enrolled before 2020 can continue to benefit from its comprehensive coverage. This includes coverage for the Part A deductible, Part B deductible, coinsurance, and copayments, among other expenses. For example, if you have Plan F and incur a $1,500 hospital stay covered under Part A, Plan F would cover the Part A deductible and any coinsurance you might owe.

If you are eligible for Medicare Supplement Plan F, understanding its details is vital. Navigating the options can feel complex, so consulting with a licensed insurance agent specializing in Medicare can be immensely helpful. They can guide you through the specifics of each plan, including premiums, coverage details, and network considerations, empowering you to make well-informed decisions about your healthcare needs.

Advantages and Disadvantages of AARP Medicare Supplement Plan F

| Advantages | Disadvantages |

|---|---|

| Predictable out-of-pocket costs | No longer available to newly eligible beneficiaries |

| Comprehensive coverage | Potentially higher premiums compared to other Medigap plans |

Frequently Asked Questions about AARP Medicare Supplement Plan F:

1. Can I still get Plan F if I became eligible for Medicare after 2020? No, Plan F is not available to those newly eligible for Medicare after January 1, 2020.

2. What if I already have Plan F? You can keep your Plan F coverage.

3. What are some alternatives to Plan F? Plan G is a popular alternative, offering similar coverage except for the Part B deductible.

4. How much does Plan F cost? Premiums vary depending on factors like location and age. Contact a licensed insurance agent for specific quotes.

5. Does AARP offer other Medigap plans? Yes, AARP (through UnitedHealthcare) offers a range of Medigap plans.

6. How do I enroll in a Medigap plan? You can enroll through a licensed insurance agent or directly through an insurance company.

7. Can I switch Medigap plans? Switching plans may have certain restrictions and requirements, so consult with an insurance agent.

8. What is the difference between Medicare Advantage and Medicare Supplement? Medicare Advantage is an alternative to Original Medicare, while Medicare Supplement works alongside Original Medicare.

In conclusion, AARP Medicare Supplement Plan F, while no longer available to newly eligible Medicare beneficiaries, remains a valuable coverage option for those who enrolled before 2020. Its comprehensive benefits offer significant financial protection and peace of mind. Understanding the nuances of Plan F, including its costs, benefits, and eligibility, is essential for making informed decisions about your healthcare. While Plan F may not be an option for everyone, exploring other Medigap plans like Plan G can provide similar coverage and help you navigate the complexities of Medicare with confidence. Consult with a licensed insurance agent specializing in Medicare to determine the best plan to meet your individual healthcare needs and budget. They can provide personalized guidance and help you make the most of your Medicare benefits. Taking the time to thoroughly research and understand your options is the first step towards securing a healthy and financially secure future.

Unlocking elegance behr pewter solid color stain

Navigating arkansas health and human services

Unleash elk river mn your ultimate adventure guide