Navigating the healthcare landscape can feel like traversing a digital labyrinth, especially as we age. One particular puzzle piece that often confounds is Medicare supplemental insurance, specifically, the AARP-endorsed Plan G. This comprehensive guide aims to demystify the AARP Medicare Supplement Plan G, offering a clear roadmap to understanding its intricacies.

Imagine Medicare as the foundation of your healthcare coverage. While robust, it doesn't cover every medical expense. That's where Medigap, or Medicare Supplement insurance, like Plan G, steps in. AARP, a trusted advocate for seniors, doesn't directly offer insurance, but it endorses plans from UnitedHealthcare, adding another layer of perceived security for many.

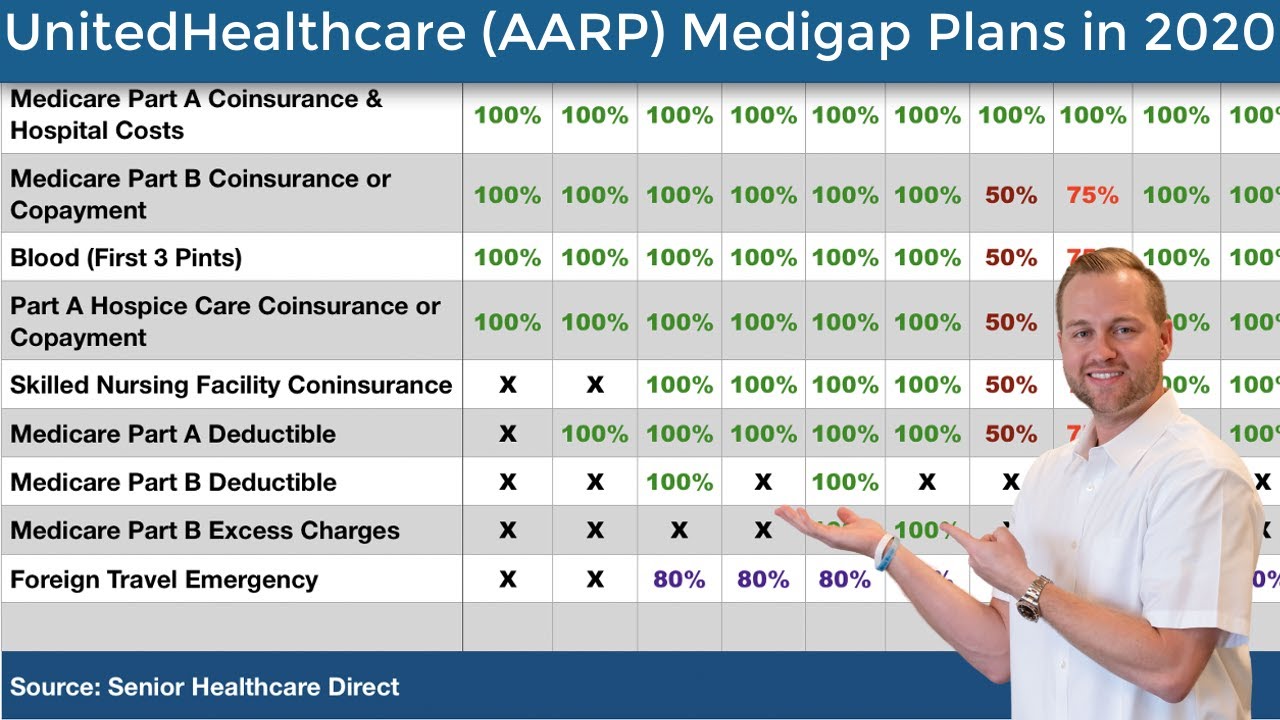

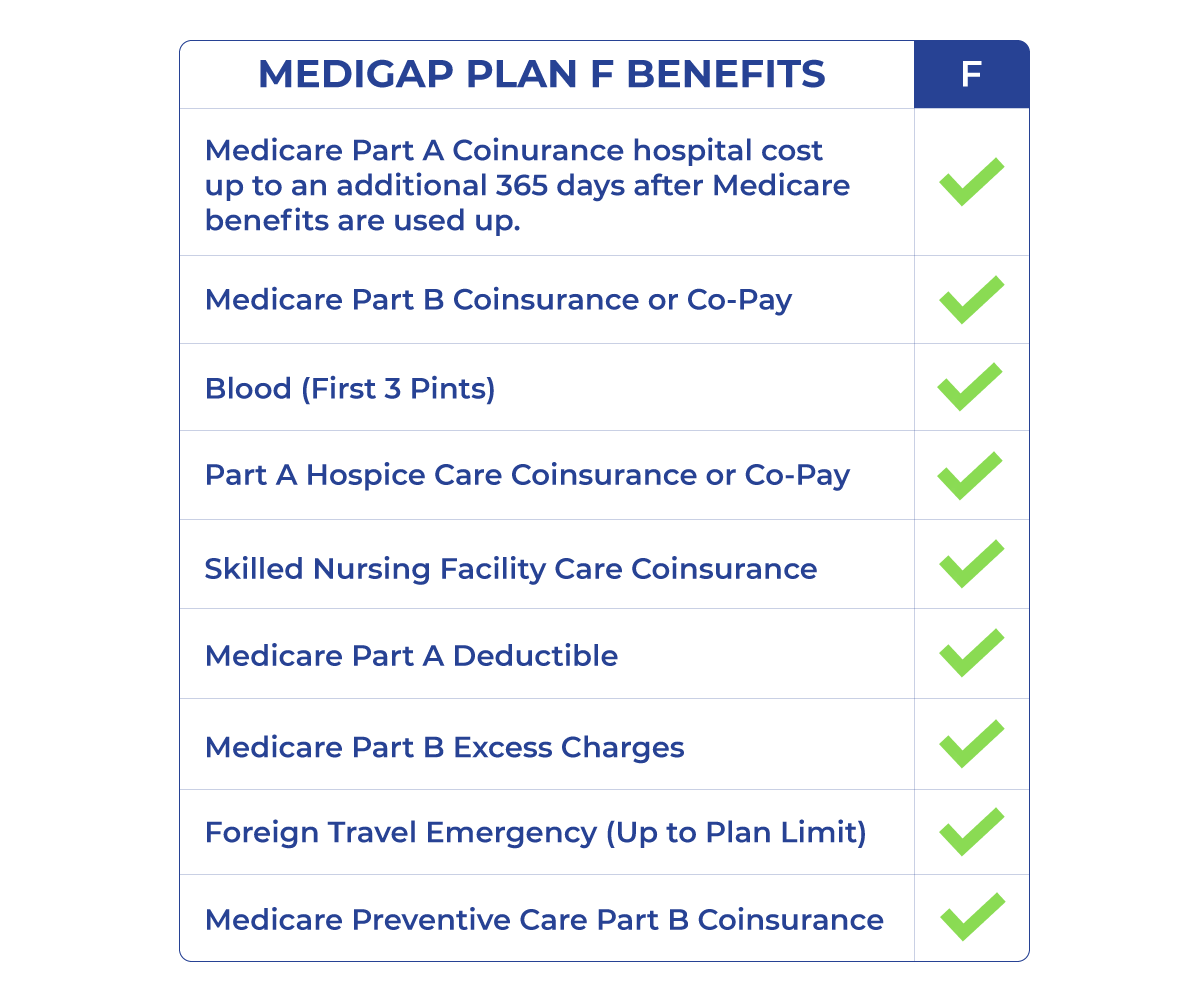

The genesis of Medigap plans like the AARP-branded Plan G stems from the recognition that Original Medicare leaves gaps in coverage. These supplemental plans are designed to plug those financial holes, mitigating out-of-pocket expenses like copayments, coinsurance, and deductibles. Plan G, in particular, has gained popularity for its comprehensive coverage, leaving beneficiaries responsible only for the Part B deductible.

One of the key issues surrounding any Medicare Supplement plan, including AARP Plan G, is understanding its true cost. Premiums can vary based on factors like location, age, and the insurance company providing the coverage. It's crucial to compare quotes from different insurers offering AARP Plan G to secure the most competitive rate.

Another consideration is eligibility. You are generally eligible for a Medicare Supplement plan during your Medigap Open Enrollment Period. This six-month window begins when you're both 65 or older and enrolled in Medicare Part B. Understanding this timeframe is paramount to avoid potential enrollment complications later on.

The AARP Plan G provides coverage for various medical expenses not fully covered by Original Medicare. This can include hospital copayments, coinsurance for doctor visits and outpatient services, and even coverage for some medical care received outside the United States. It's important to note that, while Plan G covers Part A hospital costs, the Part B deductible remains the beneficiary's responsibility.

Choosing a Medigap plan requires diligent research. Compare AARP Plan G with other options, like Plan N, considering factors like coverage and cost. For instance, Plan N might have lower premiums but requires copays for doctor visits and emergency room visits that are not deemed emergencies.

Benefit 1: Predictable Healthcare Costs: By covering most out-of-pocket expenses, Plan G offers financial predictability. Example: A hospital stay exceeding the Medicare Part A benefit period is covered by Plan G, minimizing unexpected bills.

Benefit 2: Travel Coverage: Plan G provides some coverage for emergency care received outside the US. Example: If you experience a medical emergency while traveling abroad, Plan G can help offset the cost.

Benefit 3: Peace of Mind: Knowing you have comprehensive coverage can provide significant peace of mind. Example: A sudden illness requiring extensive medical care won't cause overwhelming financial stress.

Advantages and Disadvantages of AARP Plan G

| Advantages | Disadvantages |

|---|---|

| Comprehensive Coverage | Higher Premiums compared to other plans |

| Predictable out-of-pocket costs | Doesn't cover the Part B deductible |

| Foreign travel emergency coverage | May not be the most cost-effective option for everyone |

FAQ:

1. What does AARP Plan G cover? - Answer: Most out-of-pocket costs except for the Part B deductible.

2. How much does AARP Plan G cost? - Answer: Varies based on location, age, and the insurance carrier.

3. When can I enroll in AARP Plan G? - Answer: During the Medigap Open Enrollment Period.

4. What is the difference between AARP Plan G and Plan N? - Answer: Plan G offers more comprehensive coverage but comes with higher premiums.

5. Does AARP Plan G cover prescription drugs? - Answer: No, Part D covers prescription drugs.

6. Can I switch from one AARP Medicare Supplement plan to another? - Answer: Yes, you may be able to switch plans, but underwriting may apply.

7. What are the best practices for choosing a Medigap plan? - Answer: Compare plans, consider your budget and healthcare needs, and research insurance companies.

8. Does AARP directly provide insurance? - Answer: No, AARP endorses plans from UnitedHealthcare.

Tip: Contact several insurance companies offering AARP Plan G to compare quotes and coverage details.

In conclusion, navigating the world of Medicare Supplement plans can be complex. However, by understanding the nuances of the AARP Medicare Supplement Plan G, you can make informed decisions about your healthcare coverage. Plan G provides comprehensive coverage, offering financial predictability and peace of mind, albeit at a higher premium. Weighing the advantages and disadvantages, considering your individual needs and budget, and diligently comparing quotes will empower you to choose the optimal supplemental coverage to complement your Medicare benefits. Taking proactive steps to understand your healthcare options is an investment in your future well-being, allowing you to navigate the healthcare landscape with confidence and clarity. Don't hesitate to consult with a licensed insurance agent or visit the Medicare website for personalized guidance. Your health and financial security are worth the effort.

Finding the best deals on brita maxtra water filters

Crafting the perfect educational background showcase

Sherwin williams white with brown undertone the lowdown