Medicare can feel like a complex maze, leaving many seniors wondering how to navigate the various coverage options. For those seeking enhanced protection beyond original Medicare, AARP-endorsed Medicare Supplement Insurance plans, offered by UnitedHealthcare Insurance Company, can provide an added layer of security. But what exactly are these supplemental plans, and how can they benefit you?

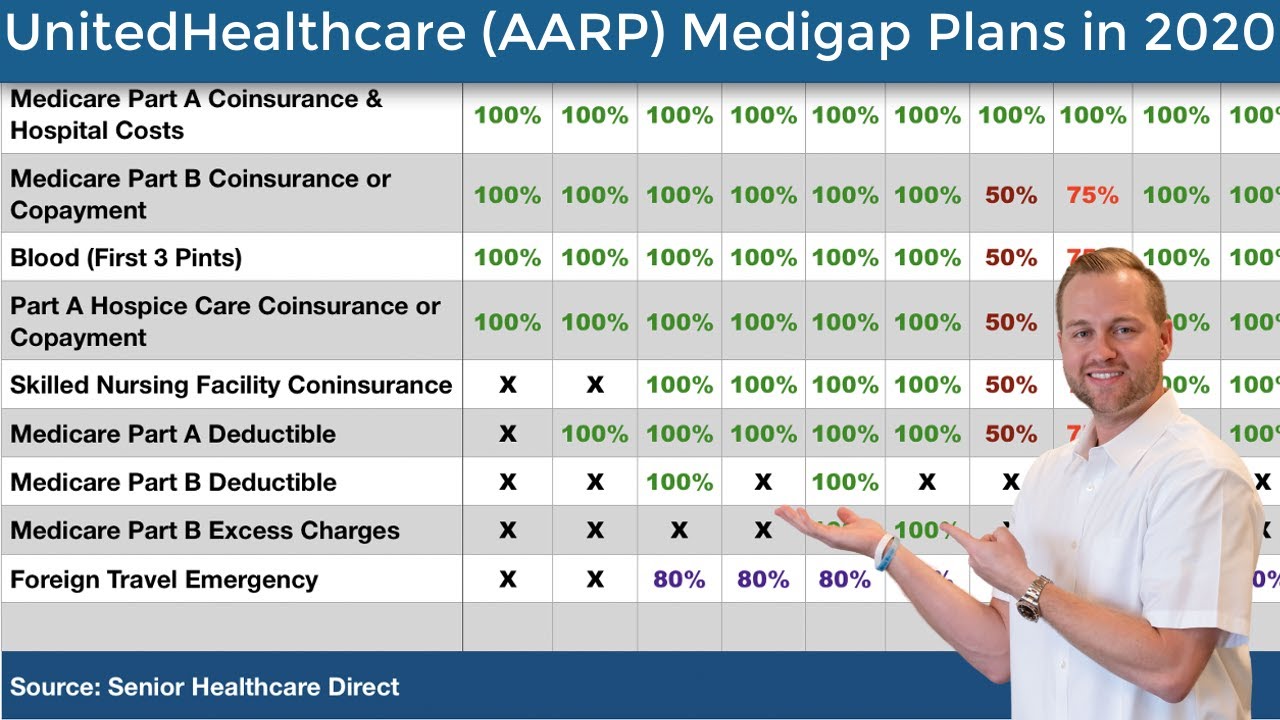

AARP health care supplement plans, also known as Medigap policies, are designed to fill the gaps in original Medicare coverage. They help pay for some of the out-of-pocket costs that Medicare Part A and Part B don't cover, like copayments, coinsurance, and deductibles. This can be especially important for individuals who anticipate significant medical expenses. These plans are standardized and identified by letters (like Plan G, Plan N, etc.), offering predictable coverage across different providers.

The history of Medicare Supplement Insurance is intertwined with the growth of Medicare itself. As Medicare evolved, the need for supplemental coverage became apparent, leading to the standardization of Medigap plans in the 1990s. AARP, recognizing this need, partnered with UnitedHealthcare to offer these plans to its members. The availability of these supplemental plans has become an important factor for retirees in managing health care costs. One main issue related to AARP supplement plans revolves around choosing the right plan based on individual needs and budget, since coverage options and premiums vary.

Let's take a simple example. Imagine a scenario where an individual incurs a hospital bill of $10,000. Medicare Part A might cover a significant portion, but the beneficiary could still be responsible for a deductible and coinsurance. An AARP Medicare Supplement Plan could then step in to cover some or all of these remaining costs, depending on the specific plan chosen, providing financial relief and peace of mind.

Understanding the alphabet soup of plan options is crucial. Plan G, for instance, offers comprehensive coverage for most Medicare-approved expenses, while Plan N offers a balance of coverage and affordability by requiring copays for certain doctor visits and emergency room services. Navigating these options can be daunting, which is why consulting with a licensed insurance agent or using online resources can be beneficial.

Three key benefits of AARP health care supplement plans include predictable costs, freedom to choose any doctor who accepts Medicare, and nationwide coverage. Predictable costs are achieved through standardized plan benefits. The freedom to choose any Medicare-accepting doctor eliminates network restrictions, providing flexibility. Nationwide coverage means you can access your benefits anywhere in the U.S.

Advantages and Disadvantages of AARP Health Care Supplement Plans

| Advantages | Disadvantages |

|---|---|

| Predictable Costs | Monthly Premiums |

| Freedom to Choose Doctors | Cost Considerations |

| Nationwide Coverage | Not Covering all out-of-pocket costs (depending on the plan) |

Best Practices

1. Compare plans: Don't just choose the first plan you see. Compare coverage and premiums.

2. Consider your health needs: If you anticipate frequent doctor visits, a plan with low copays might be preferable.

3. Budget appropriately: Factor premium costs into your monthly expenses.

4. Review your plan annually: Your needs may change, so reassess your plan each year.

5. Seek professional advice: Talk to a licensed insurance agent or use online comparison tools.

Frequently Asked Questions

1. What is the difference between Medicare Supplement and Medicare Advantage? (Medicare Advantage plans are an alternative to Original Medicare, while supplement plans work with Original Medicare.)

2. How much do AARP supplement plans cost? (Costs vary depending on the plan and location.)

3. Can I switch plans? (You can switch plans during the Medicare Open Enrollment Period or under certain circumstances.)

4. Are there waiting periods for coverage? (There may be waiting periods for pre-existing conditions.)

5. Does AARP offer other insurance products? (Yes, AARP offers a range of insurance products.)

6. Where can I find more information on AARP plans? (Visit the AARP website or contact UnitedHealthcare.)

7. Can I keep my current doctor with an AARP plan? (Yes, as long as they accept Medicare assignment.)

8. How do I enroll in an AARP Medicare Supplement plan? (Contact UnitedHealthcare or a licensed insurance agent.)

Tips and Tricks: Research plan options online. Compare quotes from different insurers. Talk to your doctor or family members about their experiences. Attend informational seminars on Medicare and supplemental coverage. Utilize AARP’s online resources.

In conclusion, navigating the complexities of Medicare can be a daunting task. AARP health care supplement plans offer a valuable resource for individuals seeking enhanced coverage and peace of mind. By understanding the various plan options, comparing costs and benefits, and considering individual health needs, individuals can make informed decisions about their health care coverage. These supplemental plans offer an important safety net, helping beneficiaries manage out-of-pocket costs and access the care they need. Taking the time to research, compare, and choose the right plan is an investment in your health and financial well-being. Talk to a licensed insurance agent today to learn more and take control of your Medicare journey. Don't wait, secure the coverage you deserve for a healthier future. Remember, choosing the right plan can significantly impact your health care experience and financial security during retirement, making it an essential decision for every Medicare beneficiary.

Unleash your inner interior designer sherwin williams gray green paint colors

Unlocking durbans automotive gems your guide to bank repossessed cars

Decoding the 12 inch bolt the nut that fits