Navigating the complexities of healthcare coverage can be daunting, especially as we age. For many seniors, Medicare provides a crucial foundation, but it doesn't cover all medical expenses. This is where Medicare Supplement insurance, also known as Medigap, comes into play. Among the various Medigap plans, AARP Plan G stands out for its comprehensive coverage. Let's explore the advantages of this plan and how it can provide peace of mind in managing healthcare costs.

Understanding the nuances of AARP Plan G benefits is crucial for informed decision-making. This plan offers extensive coverage for various medical expenses, including hospital co-pays, coinsurance, and Part A deductibles. It essentially fills the gaps left by Original Medicare, reducing your financial burden significantly. This comprehensive coverage is a key reason why Plan G is a popular choice among seniors.

The history of Medigap plans is intertwined with the evolution of Medicare itself. As Medicare beneficiaries faced increasing out-of-pocket costs, the need for supplementary coverage became evident. Over time, standardized Medigap plans, including Plan G, emerged to offer clarity and consistency in coverage. AARP, a prominent advocacy group for seniors, partnered with UnitedHealthcare to offer Plan G, leveraging its trusted name and extensive network.

One of the primary issues addressed by AARP Supplement Plan G is the unpredictability of healthcare expenses. While Medicare covers a substantial portion of medical costs, certain expenses, like coinsurance and copayments, can still be significant. Plan G effectively mitigates these expenses, providing predictable and manageable out-of-pocket costs. This predictability allows seniors to budget more effectively and avoid unexpected financial strain.

AARP Medigap Plan G helps address potential gaps in Original Medicare coverage, offering peace of mind and financial protection for various healthcare services. For instance, it covers Part A hospital coinsurance and copayments after Medicare benefits are exhausted. This protection ensures that even extended hospital stays are financially manageable. Furthermore, Plan G covers the Part B coinsurance, reducing the cost of doctor visits, outpatient services, and other essential medical care.

Three key advantages of AARP Plan G include predictable out-of-pocket costs, comprehensive coverage, and access to a broad network of providers. For example, if you incur significant hospital expenses, Plan G covers the coinsurance and copays, leaving you with a predictable and manageable out-of-pocket expense. This predictability allows for better financial planning and reduces the stress associated with unexpected medical bills.

When considering AARP Plan G, compare quotes from different insurance companies offering the plan. Review the policy details carefully, paying attention to coverage limitations and exclusions. Discuss your healthcare needs and budget with a licensed insurance agent to ensure that Plan G aligns with your individual circumstances.

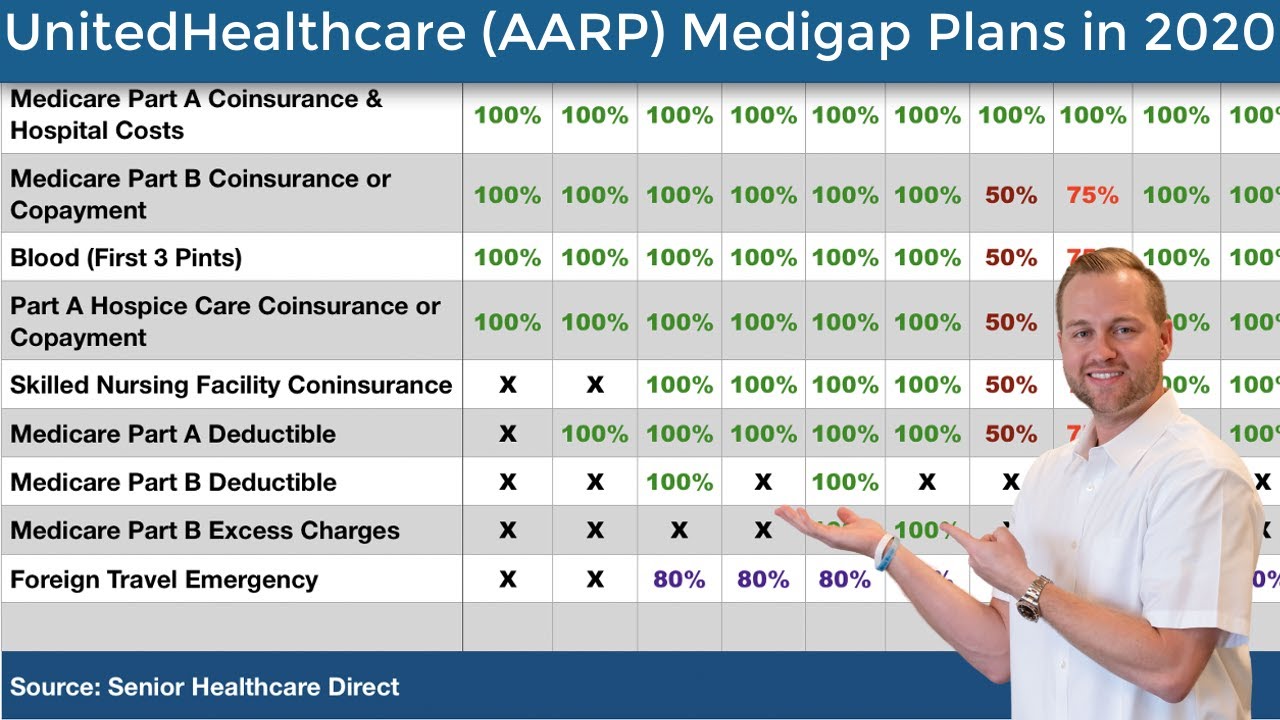

Advantages and Disadvantages of AARP Plan G

| Advantages | Disadvantages |

|---|---|

| Comprehensive Coverage | Higher Premiums |

| Predictable Costs | Doesn't Cover Part B Deductible |

Frequently Asked Questions (FAQs)

Q: What does AARP Plan G cover? A: AARP Plan G covers most out-of-pocket expenses not covered by Original Medicare, such as Part A and Part B coinsurance and copayments.

Q: Who is eligible for AARP Plan G? A: Individuals enrolled in Medicare Parts A and B are generally eligible for AARP Plan G.

Q: How do I enroll in AARP Plan G? A: You can enroll in AARP Plan G through a licensed insurance agent or directly through UnitedHealthcare.

Q: How much does AARP Plan G cost? A: The cost of AARP Plan G varies based on factors such as age, location, and the specific insurance company.

Q: What is the difference between AARP Plan G and other Medigap plans? A: Medigap plans are standardized, offering similar benefits. AARP partners with UnitedHealthcare to offer Plan G.

Q: Can I switch from one Medigap plan to another? A: You may be able to switch plans during certain enrollment periods.

Q: What are the limitations of AARP Plan G? A: AARP Plan G does not cover the Part B deductible.

Q: Does AARP Plan G cover prescription drugs? A: No, you will need a separate Part D prescription drug plan.

In conclusion, AARP Supplement Plan G offers a valuable layer of financial security for seniors navigating the complexities of healthcare costs. Its comprehensive coverage, predictable expenses, and access to a wide network of providers make it a compelling option. By carefully evaluating your individual needs, budget, and available resources, you can make an informed decision about whether AARP Plan G is the right choice to supplement your Original Medicare coverage and secure your financial well-being. Remember to compare quotes, consult with licensed insurance professionals, and prioritize your healthcare needs when making this important decision. Understanding the complexities and benefits of the AARP Supplement Plan G empowers individuals to take control of their healthcare expenses and embrace a more secure financial future.

Afton family reactions to michael a deep dive

Conquering the california driving exam your roadmap to success

Find your ideal toyota rav4 in johannesburg